From my average cost, my Alibaba position has an unrealized loss of 44% (January 2022) which is approximately $315,000 of my capital. However, I'm not discouraged about my investment and keep holding my shares for a long-term play. I'm going to keep purchasing more Alibaba shares with the dividends I will receive from Pfizer Inc. (Ticker: PFE) and my rental income.

Yes, it's true that if I had stuck with my previous portfolio, my stock portfolio would have $1,350,000. That's approximately $350,000 difference. I learned my lesson that sometimes it's better to be diversified. Luckily, I'm not using options that have an expiry date for holding a particular stock. So even if my stock portfolio is doing poorly at the moment, I know I still can make money in the long run. In this article, I will explain why I'm going to keep holding to my Alibaba stock and why I think the fallen price is an excellent opportunity to purchase more shares of Alibaba stock.

Reflecting on the Past 6+ Months of BABA's Downward Spiral.

Despite being ambiguous and cautious in earlier articles regarding the hazards of investing in BABA and Chinese equities and wary of the short-term downside risks, I eventually chose to remain hopeful. One of my bullish findings' significant flaws, I feel, was that I didn't properly acknowledge the significance of investor psychology and how others would interpret the same occurrences. Many investors would go for easy storylines rather than putting things in perspective (after all, it takes effort).

VIEs and later developments have been seen negatively by the market, even though the market might have ignored them. To make matters worse, new events might drastically alter the risk-reward profile; as a result, one must be willing to change one's mind on a dime, or at the very least modify exposure accordingly, when the evidence suggests it is necessary. For example, while there are some justifications for the education sector crackdown or DiDi's listing/delisting mess, the optics were not good - these events added to an already-existing climate of confusion/anxiety.

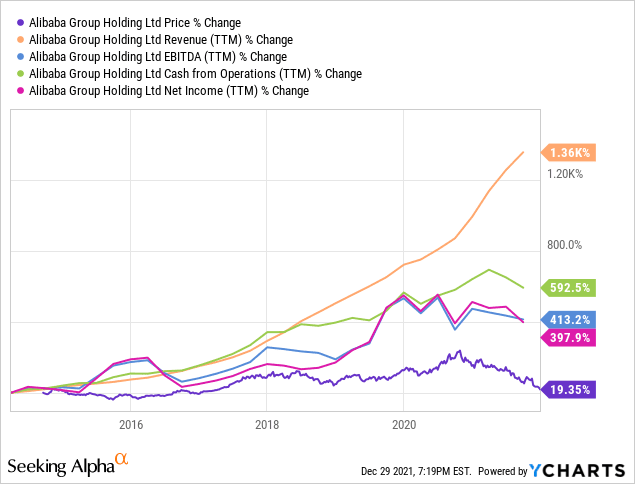

Compared to a "cowboy business culture" that may have existed in prior years, anti-monopoly measures and other rules pose new hurdles. One popular theory is that the CCP wishes to stifle significant Chinese tech firms to prevent them from becoming too big and powerful. However, if Beijing/the CCP/regulators intend to dismantle Alibaba, they'd better get to work: the stock price is now just above 2015 levels, but revenues are still up over 1000 percent, and EBITDA, cash from operations, and net income are all up around 4x or more. Overall, the regulatory environment has seemed to calm down in 2021H2, even as the stock price has continued to decline.

Alibaba's fundamentals and valuation are signaling that it's drastically undervalued.

The underlying fundamental and financial parameters are the most robust business performance indicators. Although the headlines haven't been kind to BABA, the numbers tell different stories. BABA has continued to thrive despite the stock's decline. BABA's revenue climbed 15.44 percent year over year to $126.37 billion, while its gross profit increased by $3.56 billion (7.84 percent) year over year to $3.56 billion. In terms of pure numbers, BABA appears to be undervalued more than ever compared to major tech in the United States.

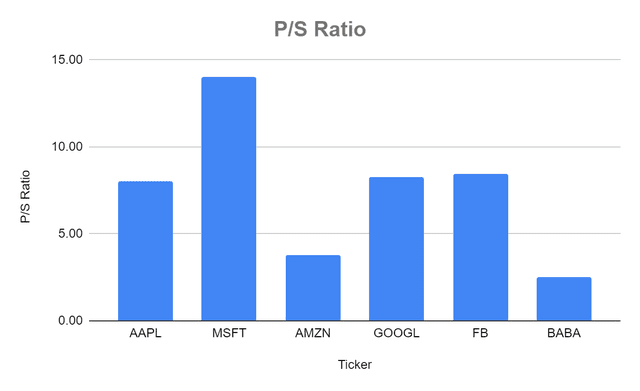

BABA is selling at a 2.4x P/S ratio, with revenue per share of $46.69 during the last three months. Amazon (AMZN) has a 3.76 price-to-earnings ratio, whereas Apple (AAPL), Alphabet (GOOGL), Microsoft (MSFT), and Meta Platforms (FB) all have multiples of more than 8 times.

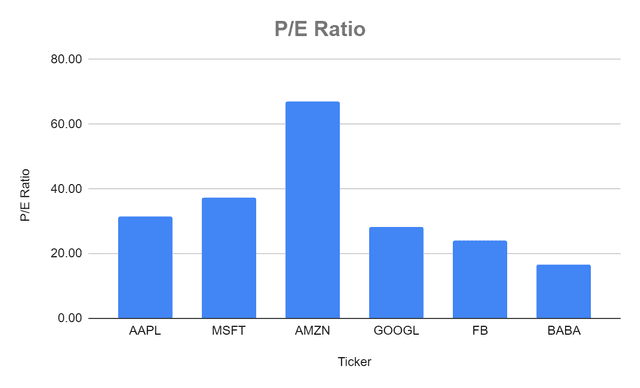

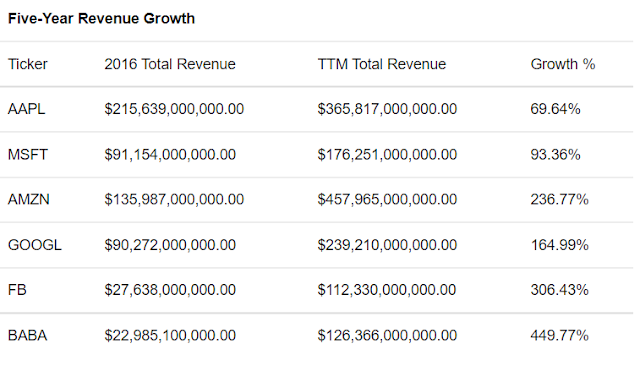

BABA has a price-to-earnings ratio of 16.74. This business has grown its sales by $16.9 billion year over year and by $103.38 billion in the last five years. BABA's EPS has climbed by 179.14 percent ($4.55). Although this isn't a slow-growth company, the P/E appears to be an industrial or utility company. FB has a price-to-earnings ratio of 23.96, while GOOGL has a price-to-earnings ratio of 28.3. The stock with the most similarities to BABA is AMZN, which trades at a P/E of 66.90. At its current price, BABA appears to be a bargain.

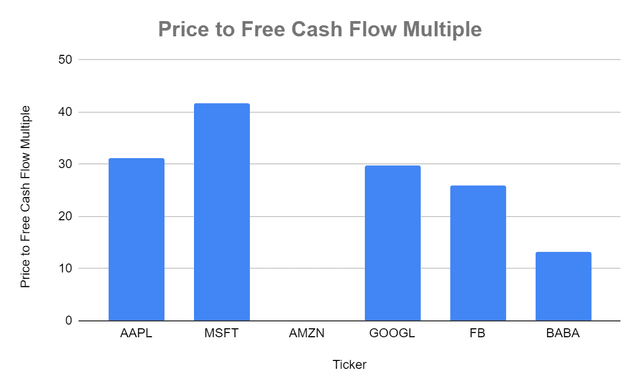

BABA generates tens of billions of dollars in free cash flow and trades at a low multiple. BABA has generated $24.09 billion in FCF over the last three months, putting its price to FCF at 13.26x. This is about half the price of Facebook, which trades at a 26.04x multiple.

The market has assigned a low multiple to BABA's stock, now trading at 1.88x. With a market capitalization of $319.37 billion, BABA has $170.25 billion in equity. The market is significantly underestimating BABA's equity on the books based on its revenue growth and the FCF it generates. FB has a 6.99x multiple, whereas GOOGL has a 7.99x multiple.

BABA appears to be a low single-digit growth firm, with a P/E of 16.74 and a P/S of 2.54. Over the last five years, BABA's income has climbed from 449.77 percent ($103 billion) to $126.37 billion. This is precisely what a corporation with a P/E of 16.74 and a P/S of 2.54 would have produced. Over the same time period, Facebook's revenue increased by 306.43 percent to $112.33 billion. When investors were flocking to growth stocks, the headlines kept them away from BABA, which was one of the market's largest major tech growth businesses.

Despite the fact that the CCP's measures have not been friendly to BABA, the company continues to thrive. There is much uncertainty right now, but it will pass. BABA continues to grow at a double-digit rate year over year and generates tens of billions in free cash flow to fund its strategic investments. BABA has generated $24.09 billion in FCF and $19.34 billion in net income over the last three months. BABA shares are currently trading at 13.26x FCF, 1.88x equity, a P/E of 16.74, and a P/S of 2.54. The fundamentals and growth indicators of BABA favor a higher stock price. There's no reason why BABA shouldn't be one of the biggest winners as China's economy grows and more infrastructure investments are made. There are significant dangers associated with investing in Chinese companies, and investors may face greater instability, but if you're prepared to take a chance, BABA is looking like a deep value play today.

China is once again slamming the brakes on BABA, escalating the dangers of delisting to cloud.

I can't foretell the future; therefore, I'm approaching BABA as though it'll be delisted at this time. The news of BABA's delisting has dominated the media, instilling dread in the investing community. BABA's delisting doesn't bother me, and I don't believe anyone has looked into what this means. My recommendation is to phone your brokerage firm for 5-10 minutes and ask them what will happen to your shares if BABA is delisted in the future. My brokerage business informed me that if BABA is delisted, you will be able to buy BABA shares on the Hong Kong exchange. If this happens, the most pressing concern will be how quickly you will be able to access your funds if you decide to sell. When you hit sell in the present structure, the funds are instantaneously available to move into another security or take a few days to clear if you want to withdraw the money from your account. If BABA is traded on the Hong Kong exchange, it could take 3-5 weeks to receive your money. What difference does it make which exchange your BABA shares trade on if you believe in the company and don't want funds on short notice?

China's Ministry of Industry and Information Technology (MIIT) recently discontinued a relationship with Alibaba Cloud due to cybersecurity concerns. The relationship was terminated because BABA failed to notify the MIIT about vulnerabilities discovered in Apache Log4j2, an open-source logging framework. The keyword is paused, which is distinct from terminated. On the plus side, China's MIIT will re-evaluate the situation in six months, and it has been suggested that the relationship could be revived if BABA executes internal security improvements. This report may contribute to investors' poor perception of BABA as a short-term investment. This issue may be resolved by the summer of 2022, but there's little doubt that this news adds to BABA's growing list of challenges.

The MIIT story is the most recent in a long series of conflicts with the CCP. BABA was fined $2.75 billion for anti-monopoly crimes earlier in 2021. The Ant Group's IPO was canceled, and BABA's CEO, Jack Ma, went missing for several months. Earlier this year, the Wall Street Journal reported that The Ant Group was talking to the Chinese government about exchanging consumer data as part of a new credit-scoring business. The CCP also flexed its financial powers, squeezing BABA for 100 billion yuan ($15.5 billion) over five years to support Xi Jinping's vision of common prosperity.

With the CCP, you never know what you'll get next, and BABA has always been a target. The CCP's headwinds have combined with macroeconomic variables that have also influenced BABA's business. BABA recently decreased its revenue prediction for 2022, guiding for a 20-23 percent increase vs. a previous forecast of 28.49 percent. Less revenue translates to less profit, which FCF and the street despise. This will also lower earnings per share (EPS) and revenue per share (RPS). Even though BABA expects to raise income by 20% or more, it is still considered a cut. BABA has created a level of uncertainty due to decreased projections and being on the losing end of the CCP.

BABA has been a falling knife, and some may consider the current stock price a complete catastrophe. What has changed in BABA's aside from the frenzy over being delisted and a few run-ins with the CCP? When BABA's stock was trading above $300, these issues were considered possible risk considerations. The possibility of being delisted was raised, the VIE structure was questioned, and the CCP was debating technology limits and indicating that fines would be distributed more aggressively. In 2020, these were real threats, but BABA's stock was rising. The negative news is being pushed at a higher rate now that BABA's stock is declining, and there are more headlines concerning delisting and fines, which everyone who invested in BABA should have been aware of. Nothing has changed in the core business, and despite a lower forecast, BABA continues to make strategic investments and expand.

Conclusion

Being a BABA investor is difficult. While there are numerous reasons to admit failure and save the remaining investment funds, there are various reasons to be patient and wait. The only thing that remains constant is the encounters with the CCP. BABA is predicted to increase its revenue by at least 20% this year, and each of its markets is expected to see significant growth. The worldwide e-commerce business is predicted to grow by $1.5 trillion (30.61 percent) to $6.39 trillion over the next three years, accounting for only 21.8 percent of all retail. By 2030, the worldwide cloud service industry is predicted to grow at a 15.8% CAGR to $1.62 trillion.

I was mistaken about BABA, and it was a terrible investment. BABA is, in my opinion, far too vital to China's economy, and its infrastructure will be required to support the country's domestic growth. I would sell for tax-loss harvesting and move on if BABA's fundamentals and financials differed. BABA's price is far too attractive, and the company is still growing. With the last run down, I intend to increase my position. I'm not sure when I'll reach my breaking point, but BABA could be a bright spot in 2022. Only time will tell if this is true.

Every investor must decide whether or not they feel BABA shares can recover from their current negative trend. Making a call to my brokerage business and learning precisely what would happen if BABA was delisted was quite reassuring. BABA is a huge value pick, in my opinion. The CCP putting pressure on Alibaba Cloud and BABA being delisted are the two biggest concerns I see. In my opinion, BABA's strategic investments, growth, present valuation, and rising total addressable markets outweigh the negative news. If shares are delisted, I will still own BABA on the Hong Kong exchange. Today, you may buy shares in a firm that has grown its revenue by 449.77 percent ($103 billion) in the last five years and generates tens of billions in free cash flow and net income for a price of 13.26x FCF, 1.88x equity at a P/E of 16.74, and a price-to-sales ratio of 2.54.

Good explanation for readers.

ReplyDeleteA similar gaming system is available on Game. Read More

Ardent cybersecurity enthusiasts value steghide for its powerful steganography capability that hides data inside images and audio files securely while preserving file integrity making it useful for privacy focused communication and advanced digital security research applications across different environments effectively

ReplyDelete