It's practically

hard to anticipate the market's performance in any given year. Furthermore,

putting together a portfolio that yields market-beating returns is extremely

tough for an individual. In 2020, 60.3 percent of large-cap equity fund

managers underperformed the S&P 500 (GSPC), according to new data from

S&P Dow Jones Indices. This is the 11th year in a row that professionals

have fallen short of the mark.

This is not exactly breaking news to many investors. Moreover, thanks to the likes of Warren Buffett and Jack Bogle promoting the benefits of investing in less expensive, passively managed index funds, S&P estimates that there are $11.2 trillion in S&P 500 index funds. To be fair, many active fund managers are not simply seeking to outperform the S&P 500; they're also trying to provide investors with risk exposures that aren't replicated by the benchmark index.

This is an exciting topic to talk about. I wondered if it's better to let a professional fund manager manage my portfolio or whether it's better to manage my own. When I came back from the United States to Jakarta, Indonesia, My father did give me some capital to start with. I invested some of the money into Mutual Funds managed by professionals. The result is not very exciting; the portfolio that fund managers manage did worse than the stock portfolio I built from scratch. In this article, I will explain whether it is better to invest on your own or pay a fund manager to do the job for you. Moreover, I will explain my experience as a stock investor and why you should just invest in a low-cost index fund such as S&P500 (Ticker: SPY) if you are still a beginner in the investing world.

Is it Better to Do Your Own Investing or Hire a Fund Manager?

Everyone wishes to profit from the stock market. That is what investing is all about. The S&P 500 and the Dow Jones Industrial Average are two popular indexes that investors use to gain a broad picture of how the stock market is behaving.

The S&P 500 is a market capitalization index that includes the 500 largest publicly traded firms in the United States. The Dow Jones Industrial Average, on the other hand, is a stock market index that follows the stock prices of 30 of the largest American corporations.

Because everything is relative, investors compare their assets to these two indexes, particularly the S&P 500, representing a broader slice of Wall Street. Your goal may not be to outperform the S&P 500 in any particular year, but it is a valuable indicator of how well your investments perform.

Many investors, once again, lack the confidence to invest on their own, so they pay a fund manager to handle it for them. Especially during times of turbulence, fund managers are educated to invest your money and obtain the best available terms.

Is there a fee charged by active Fund Managers?

You must pay the price to participate in this experience. The average cost in Canada is roughly 2.3 percent. If you have a $100,000 investment portfolio, they will deduct $2,300 from your earnings each year. If your portfolio grows by 4.6 percent, you will be back to where you started in a year.

It turns out that investing on your own may be a superior option. According to S&P Dow Jones Indices, in 2020, 60.3 percent of large-cap equities fund managers would underperform the S&P 500. This is the eighth year in a row that professional fund managers have underperformed the benchmark.

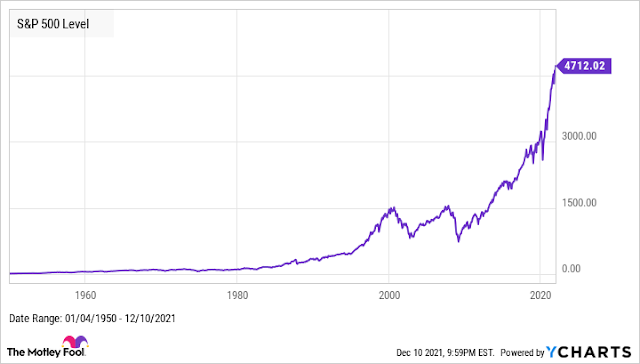

One of the main reasons why active fund managers advise you to trust them with your money is that they claim to be able to outperform you, particularly during periods of high volatility. Well, there was plenty of that in 2020. The S&P 500 index began 2020 at all-time highs, but between February 19 and March 23, it plummeted 33.8 percent.

Despite confronting the worst economic crisis since the Great Depression and the worst health crisis in a century, the S&P 500 rallied to a new all-time high in August and ended the year up 18.4%.

Everyone wants to

beat the S&P 500, even if active fund managers don't set out to do so. It

demonstrates that you are wiser than Wall Street and Bay Street. As a result,

fund managers would typically focus on stocks in the S&P 500 while also

looking for exposure to equities outside the index. They'll also make changes

to their portfolio to take advantage of new chances.

This means they should be approaching or exceeding the S&P 500 on a regular basis. They aren't, however. On the other hand, active fund managers are more likely to underperform the S&P 500.

This means they should be approaching or exceeding the S&P 500 on a regular basis. They aren't, however. On the other hand, active fund managers are more likely to underperform the S&P 500.

The majority of active investment managers do not outperform the S&P 500 index.

What does this mean in terms of active vs. passive, indexed investing? The S&P 500 has been on a tear for more than a decade. Few market segments have kept up with it, whether in the stock, bond, or commodity markets. Those poor active managers can't seem to get a break in such a situation unless they have smuggled a few tech behemoths into their stock portfolios and kept them there.

This, however, is merely a diversion from the truth. Most active managers haven't beaten the S&P 500 Index in the last three, five, or ten years because they aren't attempting to do so. And even if they tried, they'd probably be out of business in no time.

The Causes of Active Fund Managers' Failure

While the low results are stunning on the one hand, they are not wholly unexpected. The poor performance of active funds can be traced back to several factors.

The financial markets have experienced a professionalization process since the 1960s, resulting in a hyper-educated, hyper-competitive industry. Portfolio management is a zero-sum game in which fund managers must out-skill one another to profit. What's the result? The average active fund manager does not have a competitive advantage in his or her market.

Active fund managers could succeed in a less professional or educated market. Being one of the 15-25 percent that beats passive funds is extremely difficult, as indicated by the SPIVA scorecards.

Long-Term Problems

Active funds also have disadvantages that limit their ability to weather the ups and downs of long-term performance. Long-term stock market success frequently necessitates the determination to hold on to an underperforming stock but has significant promise in the short run. During these downturns, though, it's easy to lose investor trust - and your fund management job.

Furthermore, according to this study, funds that surpass their benchmark for 15 years spend 60-80% of that time underperforming. These figures necessitate a strong will and investor awareness.

I say all of this not to imply that active fund managers are buffoons who are so inept that they can't beat the market — although some experts, such as David Blake of Cass Business School, believe so.

On the contrary, these are brilliant folks trapped in a difficult trading discipline. However, regardless of the understandable reasons, their fitness for smart pension investing must be questioned.

Other Causes of Poor Performance

Fees and taxes are two more elements that influence active fund performance.

Taxes

To make a profit, active funds must time the market. Transaction fees affect the fund's returns when buying and selling. Profits also result in capital gains, passed on to the shareholder.

Fees

Fees eat down the returns of active funds. Management fees for mutual funds range from 1-2 percent each year, compared to 0.1-0.2 percent for passive indexing. You may be charged sales costs when you buy or sell the fund, which typically ranges from 4 to 8%. These fees accumulate over time and have a negative impact on returns.

What's the Alternative to Investing on Your Own!?

Buffett recommended investing in a low-cost index fund instead of picking stocks. "I have recommended the S&P 500 index fund to people for a long, long time," Buffett remarked, referring to a fund that includes 500 of the country's largest companies.

Buffett illustrated his argument with a slide depicting the enormous number of automotive businesses in the early 1900s. "At least 2,000 firms entered the car industry because it had this great potential," he remarked. "And by 2009, only three remained, two of which had gone bankrupt." Buffett stated, "It's a wonderful argument for index funds." "If you just had a diversified bunch of equities, U.S. equities, that would be my preference, but over 30 years," he says.

After he dies, Buffett has asked the trustee in charge of his estate to invest 90% of his money in the S&P 500 and 10% in treasury notes for his wife. "I believe that buying 90% of an S&P 500 index fund is the smartest thing to do."

My Opinion for Beginners who wants to build wealth.

Suppose you are still new to the investing world. You should just invest your money in a low-cost index fund, as Warren Buffett suggested. I have been in the investing world for quite some time already, and still, I underperform the S&P500 when comparing the portfolio I am currently managing. Instead of wasting your time trying to outperform the market, you should focus more on increasing your income stream and saving rate.

I say this is because I have been in the stock investing world for a long time (since 2007). That's approximately 15 years ago. My father gave me $350,000 USD in the capital in total. If I have invested that starting capital in a low-cost index fund such as the S&P500 (Ticker: SPY) that generates 12% annually, I would have a total of $1,900,000 USD in net worth at the current moment. That calculation is without me investing more capital into the portfolios. Currently, my personal net worth is at $1,300,000 USD, but this amount is with a monthly contribution of around $30,000 USD annually since I started working in my father's company in 2013.

If I had just invested the starting capital of $350,000 USD from my father and invested the monthly contribution to my portfolios in a low-cost index fund, I probably would have done way better than managing my portfolio. I did some calculations with the compound interest calculator; I found out that I would probably have $2,500,000 USD in overall personal net worth if I had just invested the capital given from my father and a monthly contribution of $30,000 annually since 2013. That would be a difference of $1,200,000 USD more if I had just done the simple investment advice given by Warren Buffett.

This is why I am advising beginners who want to start building wealth. I'm not saying you shouldn't learn more about investing; however, don't underestimate the power of investing in a low-cost index fund. Focus on your income stream and manage your personal finance to have a high saving rate. I believe just by managing your saving rate and having the discipline to keep investing your monthly income into the low-cost index fund; you can perform well.

Why Invest in the S&P500 Index Fund?

The Standard & Poor's 500 Index (S&P 500) is a market-capitalization-weighted index of 500 of the largest publicly traded firms in the United States. The average annual return on the S&P 500 index has been between 10% and 11% since 1926. This includes the S&P 90, which consisted of only 90 stocks from 1926 and 1957. Since 1957, when 500 stocks were adopted, the average annual return has been roughly 8%.

Due to their cost-effective technique of diversifying one's holdings over wide sectors or businesses, index funds have become one of the most popular ways to invest. In a single transaction, they purchase one share of the S&P 500 index fund equivalent to purchasing small shares in the top 500 blue-chip companies in the United States.

This index is also weighted, which means the largest stocks account for a larger percentage of the portfolio. Apple, for example, is currently the largest stock in the index, accounting for about 6% of the S&P 500. News Corporation Class B is the smallest stock in the index, accounting for only.008% of the total. So Apple is around 777 times the weight of the smallest stock, but it doesn't make it a small company. The market capitalization of News Corporation Class B, or the value of the company's equity, is $14.3 billion. You'll get exposure to these companies and other well-known names like Coca-Cola, PayPal, Disney, Home Depot, and Netflix if you invest in the S&P 500.

The S&P 500 index has grown value in 40 of the last 50 years, an excellent track record. The market has seen its fair share of ups and downs, but if you have several decades before retirement, the S&P 500 has shown to be a successful and safe investment.

Bottom Line

After reading this article, I hope readers out there understand why you shouldn't invest your hard-earned money with fund managers. I believe you should focus on your income stream and saving rate and simply invest monthly into a low-cost index fund. I learned my lesson the hard way; I would be wealthier right now if I had just followed the simple advice Warren Buffett preached. I hope readers will not make the same mistake as I did. If you are in your early 20s and have just started your career life, invest early in low-cost index funds such as the S&P500 (Ticker: SPY). Trust me! You will be a wealthy person future ahead.

Hi Hansen,

ReplyDeleteI'm totally with you on going the DIY investing route. It was my entry way into investing only 1.5 years ago and I can't say I know what it's like to be with a fund manager, but having the control of my portfolio that I have now is something I wouldn't want to give up, like ever.

Although, I do wonder what your thoughts are on ETFs, since you spoke about index funds and they are generally lower cost, ETFs have a bit of a higher cost but allow for a little more of a passive approach if you don't want to be constantly researching every stock on your own. What are your thoughts?

pusulabet

ReplyDeletesex hattı

https://izmirkizlari.com

rulet siteleri

rexbet

1CSP

pusulabet

ReplyDeletesex hattı

https://izmirkizlari.com

rulet siteleri

rexbet

AKL

https://saglamproxy.com

ReplyDeletemetin2 proxy

proxy satın al

knight online proxy

mobil proxy satın al

GWV

I admire Follower Magazine for delivering news that is both informative and forward-looking. Their articles cover technology, AI, crypto, and global developments in a way that educates and engages readers consistently.

ReplyDeleteThe website impresses with its ability to turn complex news into accessible insights. Greece Report offers clarity and perspective, ensuring readers are well-informed and can navigate the real stories behind headlines.

ReplyDeleteBuying Journal provides an impressive blend of insight, strategy, and trend analysis. The content is consistently fresh, relevant, and practical, helping readers stay informed, explore new ideas, and maintain a competitive edge in business and technology.

ReplyDeleteGood explanation for readers.

ReplyDeleteA similar gaming system is available on Game. Read More